While the Obama ‘Affordable’ Care Act (ACA) aims to decrease the number of uninsured Americans, there are many who remain without coverage for one reason or another.

Kaiser Family Foundation research found that:

- 48 percent of adults uninsured in 2014 said the main reason they lacked coverage was due to cost

- 12 percent cited work-related reasons

- 13 percent were told they were ineligible or could not get coverage due to their immigration status

- Few uninsured adults were uninsured because they said they didn’t need coverage, opposed the ACA or preferred to pay the penalty

If you are among these individuals, what impact could having no health insurance have on you?

The consequences of going uninsured widely vary based your health and finances, amongst other things. In terms of the ‘Affordable’ Care Act and its individual shared responsibility provision, going without an Obamacare plan can also have tax implications.

What are those tax implications?

It depends on your situation.

Do you qualify for an Obamacare ACA exemption?

While the ‘Affordable’ Care Act’s individual shared responsibility requires most Americans to have health insurance, there are certain situations in which exemptions are granted. Those who qualify for exemptions will not owe the shared responsibility payment for going without minimum essential coverage.

Some examples if exemption-eligible circumstances include:

– Having a gross or household income below the minimum threshold for filing a tax return

– Experiencing general hardship due to circumstances such as homelessness, foreclosure, death of a close family member, unpaid medical bills and more

– Being a resident of a state that did not expand Medicaid

Some Obamacare exemptions must be claimed or reported when you file your taxes. Others are automatic. More information is available at IRS.gov. If you believe you might qualify for an exemption, speak with your health insurance producer and/or a financial adviser.

You are allowed a single period of up to three months without ACA-compliant health insurance coverage. If you do not qualify for an exemption and have no health insurance beyond this, you could owe the shared responsibility payment.

This fee is paid when you file your federal taxes for the year in which you were not compliant with the healthcare reform law. If you went without minimum essential coverage for all or part of 2016, you would pay the Obamacare tax penalty when filing taxes for 2016.

What is the penalty for no health insurance in 2016?

The tax penalty for going without health insurance increased in 2016. It is now the greater of these amounts:

- 2.5 percent of your income above the filing threshold, capped at the national average premium for a bronze plan available through the Marketplace

- $695 per adult and $347.50 per child to a maximum family penalty of $2,085

The penalty will continue to adjust annually based on inflation and the flat dollar amounts for 2016.

No health insurance? You could benefit from short term benefits

Whether or not you are exempt from the shared responsibility provision, you might consider some other type of coverage beyond major medical insurance (i.e., an Obamacare plan) to help pay for healthcare expenses.

Short term health insurance provides temporary coverage when you are in between Obamacare plans. While these plans are not ACA-compliant and do not qualify as minimum essential coverage, they do provide a range of benefits for unexpected medical care and often have premiums that are a fraction of major medical insurance premiums.

Short term health plans last as few as 30 days and up to 364, depending on how long you think you will need temporary coverage and the laws in your state. You can apply and enroll online through websites such as www.HI4E.Org , and you can begin your coverage as soon as the next day.

Think short term. Get a quote.

* * * * * * * * * * * * * *

At Health Insurance 4 Everyone, we not only want to improve our customer service but also interact with our customers on a social media level that was not available before. Interested in connecting with us? Look us up on….

Twitter: Healthinsurane4

Click-On for LinkedIn: LinkedIn

Like us on facebook: HealthInsurance4Everyone

Follow Mark Shuster, Founder/Owner at Health & Life Solutions, LLC for daily health tips!

Mark Shuster FaceBook Link

Follow our word press blogs and read about everything from health insurance and reform news to healthy living and current events!

Company Blogs

Find out more about LegalShield, our corporate partner which gives you the power to talk to an attorney about any legal issue, and offering high-quality Identity Theft protection plans.

LegalShield

Read more

These Five (5) Questions May Hold The Answer….

Going without coverage can be tempting and even seem necessary at times, especially when you are relatively young, relatively healthy and on a relatively tight budget. However, skipping major medical coverage can also be a potentially costly decision. You may wind up owing a tax penalty (yes, even now that the Trump Administration is in office), paying unexpected medical bills out of pocket, or both.

If you are asking yourself if you really need insurance, the answers to these five questions may help you decide.

If you are asking yourself if you really need insurance, the answers to these five questions may help you decide.

1. Are you exempt from the ACA’s individual mandate?

The Obama ‘Affordable’ Care Act’s individual shared responsibility provision (aka, the individual mandate) requires most Americans to have a health plan that qualifies as minimum essential coverage. This may include, but is not limited to, job-based coverage, major medical plans purchased on and away from the state-based and federally facilitated health insurance exchanges, Medicaid and most types of TRICARE (veterans) coverage.

However, exemptions from the mandate are granted to individuals in certain circumstances, including those with coverage gaps of less than three consecutive months, those for whom coverage costs more than a certain percentage of their household income, those with incomes below the filing threshold and others facing general hardship, to name a few.

If you are not exempt and do not obtain coverage as required by the law you could face a penalty known as the shared responsibility payment at tax time.

What could being uninsured could cost you if you’re not exempt?

You may owe a tax penalty known as the individual shared responsibility payment. Those who went without minimum essential coverage in 2016 could face penalties as high as follows: that penalty could be as high as :

- 2.5% of their annual household income above the tax filing threshold to a cap of the national bronze plan s premium, or

- $695 per adult and $347.50 per child under 18 to a maximum penalty of $2,085 per family.

For every month that you are uninsured and not exempt, you owe 1/12 of the annual shared responsibility payment.

In 2017 and beyond, the penalties remain the same, but will be adjusted for inflation.

2. How will you pay for healthcare if you need it?

While we know it can happen, we never really plan on becoming ill or getting injured, especially when our medical histories are relatively spotless. If you have no benefits to help with covered expenses when you do get sick or hurt and need medical care, you will have to pay 100% of the bills out of pocket. Whether your healthcare expenses are expected or not, do you have access to savings, credit or other funds to help pay for healthcare?

What could being uninsured cost you if you need healthcare?

Insurance status has a strong association with medical bill difficulties—more than half of uninsured individuals report problems paying household medical bills. On average, a trip to urgent care will cost $150 and a trip to the emergency room will cost over $1,000. Fixing a broken leg can cost up to $7,500 and the bill for a three-day hospital stay hovers around $30,000.

3. Do you plan on being uninsured for short time?

Accidents and illnesses can happen any time, not just when it is convenient. Even if you are about to start a new job with benefits that kick in a month or two down the road, it is wise to have a plan for how you will pay for healthcare in the meantime.

Short term health insurance plans provide temporary coverage for as few as 30 days. They offer a range of benefits to help with covered expenses, including office visits and emergency care, and they can be quickly obtained. Application and enrollment take only a few minutes, and coverage begins as early as the day after you enroll. You can buy short term coverage year-round.

What could a short term health plan cost you?

Typically, short term plan premiums are a fraction of major medical premiums. Keep in mind that short term plans are not the same as Obamacare plans (i.e., major medical insurance). They are not subject to the ‘Affordable’ Care Act, which means you may be denied coverage based on your health history and, if you are not exempt from the shared responsibility provision, having short term coverage will not prevent you from owing a tax penalty.

If you plan to be uninsured longer than three months and do not qualify for a special enrollment period, you may consider a hospital indemnity plan.

Learn about HIP (Hospital Indemnity Plans)

4. Will you qualify for an Obamacare subsidy?

If you buy a major medical plan from a state-based or federally facilitated health insurance exchange (the Obamacare plans) and meet certain income qualifications, you may be eligible for a subsidy. Obamacare subsidies include advanced premium tax credits that help lower your monthly premium payment.

Remember: You can only buy major medical plans during the annual open enrollment period or during a special enrollment period if you have a qualifying life event.

What could health insurance cost you with an Obamacare subsidy?

Major medical health insurance premiums vary depending on a number of factors, including where you live, what type of plan you choose (i.e., bronze, silver, gold, platinum), and your age. In 2016, the average premium for health insurance plans purchased through the federal Obamacare HealthCare. gov exchange was $408 per month.

However, 83% of people who purchased healthinsurance through HealthCare. gov received subsidies that helped lower their monthly premiums. The average advanced premium tax credit amount was $294 per month, which lowered the average monthly cost to $113 per month.

Consider “Gap” Insurance To Cover The Higher Obamacare Plan Deductibles & Out-Of-Pocket Limits

5. Are you eligible for Medicaid?

In 2014, Medicaid eligibility was expanded to include single adults earning up to 133 percent of the federal poverty level. Not all states decided to participate in this optional expansion. You can enroll in Medicaid year-round. To view your state’s eligibility criteria, click here to visit Medicaid.gov’s State Medicaid & CHIP Profiles page.

What could Medicaid coverage cost you?

If you qualify for Medicaid, you may be able to get low-cost or no-cost coverage.

The Obama ‘Affordable’ Care Act may require you to buy health insurance, and there may be financial risks in going without it. Ultimately, you must decide if you need health insurance. It is important to understand all of the benefits and risks associated with your decision. Work with a health insurance producer to determine the right coverage  options for your health and financial situation.

options for your health and financial situation.

You can call the number at the top of your screen to speak with a certified advisor (i.e., health insurance producer) who can assist you. You can also obtain quotes for supplemental products, short term coverage and off-exchange Obamacare plans at :

HealthInsurance4Everyone – www.hi4e.org

Read more

The GOP pulled its Obamacare replacement bill before it could go to a vote on Friday, March 24th. Now what? Is that the end of Trump’s promise to repeal and replace the ‘Affordable’ Care Act (ACA) ? Will politicians draft another bill?

There are a lot of questions, and most of the answers are forthcoming. What we do know is that the ACA remains in place as written. Nothing has changed.1

Subsidies remain in effect and available to those who qualify for them. Essential health benefits will stay in place. Nobody can be denied coverage. Children may remain on a parent’s health insurance plan until age 26. The law, as written, remains the law.

The individual mandate is still in effect … but is it really?

If passed as written, the recently GOP-proposed American Health Care Act (AHCA) would have abolished the individual and employer mandates and their respective penalties, retroactive beginning with 2016.2

But the AHCA didn’t pass—again, there wasn’t even a vote—which leaves many to wonder:

Will the Trump administration enforce the shared responsibility provision, which is part of the Patient Protection and Affordable Care Act enacted on March 23, 2010 (i.e., PPACA, ACA, Obamacare)?

As consumers file their 2016 taxes, will those who went without health insurance and didn’t qualify for an exemption owe a penalty?

The existing healthcare reform law requires taxpayers to show that they have minimum essential coverage, which includes but is not limited to Medicare, Medicaid, TRICARE, CHIP, and private health insurance obtained through an employer or the individual market.3 This has not changed.

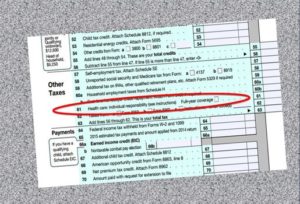

Most commonly, providing evidence of minimum essential coverage means checking a box on line 61 on page two of your individual income tax return.4 If the box goes unchecked, your tax return could be rejected—at least, that was the case until recently, and here is where some might become confused.

Will 2016 penalties be enforced this tax season?

The IRS in February stated that, starting this tax season, it will no longer systematically reject returns on which the taxpayer doesn’t indicate their coverage status.5 However, the agency may still follow up with questions. But will the IRS really enforce the individual shared responsibility payment (i.e., Obamacare tax penalty)?

Tara Straw, a senior policy analyst at the Center on Budget and Policy Priorities, in an interview with NPR reminded consumers that the individual mandate is the law and remains in effect; as such, they should pay the fine unless they qualify for an exemption.6 Straw cautioned consumers that “reputable tax preparers” would not advise them to skip the penalty or delay filing because the law could change.7

If you have questions about the individual mandate, exemptions, penalties and other tax topics related to healthcare, consult with a tax professional. The IRS also provides ACA information and resources that may be helpful but do not serve as a replacement for professional guidance.

Will there be a 2018 open enrollment?

As it has each year since the ACA’s individual mandate took effect, the open enrollment period for individual health insurance plans effective next year would begin sometime in the fall of this year. However, healthcare experts such as Mary Agnes Carey, question what the market will look like and how aggressively the Trump administration will promote it.8

This is the time of year when health insurance companies decide whether or not they will participate in the individual market and what plans they will offer.9 As the Associated Press reports, “What kinds of plans will be available and how much they will cost will depend on a few key decisions by insurers and regulators in the coming weeks.”10

What about those who need coverage now?

We encourage consumers to discuss their health insurance options with a licensed producer who can help them explore the plan types available to them.

And, again, all tax-related questions should be directed to a tax professional.

- * * * * * * * * * * * * * * * *

Visit IRS.gov for an ACA Tax Provision Q&AView IRS Help & Resources Page

1Mathews, Anna Wilde and Melanie Evans. “Health Insurers Wrestle with Next Steps as GOP Bill Fails.” The Wall Street Journal. March 24, 2017. https://www.wsj.com/articles/health-care-sector-faces-uncertainties-regardless-of-house-bills-fate-1490380594

2Hiltzik, Michael. “Column: The GOP’s Obamacare Repeal Plan is Out—And It’s Even Worse Than Anyone Expected.” LA Times. March 6, 2017. http://www.latimes.com/business/hiltzik/la-fi-hiltzik-obamacare-repeal-20170306-story.html

3Erb, Kelly Phillips. “IRS Softens on Obamacare Reporting Requirements After Trump Executive Order.” Forbes. Feb. 16, 2017. https://www.forbes.com/sites/kellyphillipserb/2017/02/16/irs-softens-on-obamacare-reporting-requirements-after-trump-executive-order

4Ibid.

5Ibid.

6Andrews, Michelle. Health Shots. “Even If You Expect Obamacare to be Repealed, Don’t Skip Paying Tax Penalty Now.” NPR. Feb. 8, 2017. http://www.npr.org/sections/health-shots/2017/02/08/513755719/even-if-you-expect-obamacare-to-be-repealed-dont-skip-paying-tax-penalty-now

7Ibid.

8Martin, Michel. All Things Considered. “What Does Failed Repeal of Affordable Care Act Mean for Current Health Care Law?” NPR. March 25, 2017. http://www.npr.org/2017/03/25/521517124/what-does-failed-repeal-of-affordable-care-act-mean-for-current-health-care-law

9The Associated Press. “Now What? Options for Consumers as Health Law Drama Fades.” The New York Times. March 25, 2017. https://www.nytimes.com/aponline/2017/03/25/us/ap-us-health-overhaul-what-now.html?_r=0

10Ibid.

Read more

In a press conference earlier in January, to announce the start of the 2017 tax filing season, which began on Jan. 23rd, the IRS said it expects more than 153 million tax returns this year.

More than 70% of taxpayers will receive a refund in 2017, with 90% or more of refunds issued in fewer than 21 days after returns are submitted, the IRS estimated. In 2016, 111 million individual tax refunds were issued.

Most filers who received government subsidies to buy Obamacare state exchange plans had to pay money back to the IRS last year, according to an H&R Block analysis released in 2016 that looks at the health law’s two full tax seasons. If a taxpayer projected a higher annual household income than they actually claimed in their filing, they may owe tax credits back that they received by purchasing an Obamacare policy or their state’s exchange plan. One other cause for having to repay tax credits is due to claiming eligibility, but not being eligible due to having access to affordable employer coverage.

The tax-prep giant studied its own massive customer base and concluded that two-thirds of its filers who got subsidies from Obamacare were overpaid during the course of the year, and owed money back to the IRS on the April 15th deadline.

The ‘Affordable’ Care Act, better known as Obamacare, mandates Americans — unless they’re qualified for an exemption — to carry health insurance coverage or pay a penalty when filing their tax returns. The IRS says most taxpayers simply need to check a box to verify that they have insurance. For others with more complex answers, the agency offers tips on IRS.gov/aca.

IRS Commissioner John Koskinen said the number of people receiving Obamacare subsidies during the last tax season (2015 tax filing), was up from 3 million in 2014. For that year, customers got more than $10 billion in tax credits, with an average subsidy of $3,430 annually, according to the IRS. Obamacare subsidies are available to wage earners with low and moderate incomes. People who earn less money get more in assistance than higher earners.

Koskinen wrote that about 6.5 million taxpayers last tax season reported owing a total of $3 billion in such tax penalties for failing to have coverage in 2015. In contrast, about 8 million people owed an Obamacare fine for lack of coverage in 2014. Fines related to lack of coverage in 2014 totaled $1.6 billion.

CNBC reported that some 12.7 million people claimed one or more exemptions from the ACA-coverage mandate when they filed their taxes last year. “The exemptions are wide ranging and can include having very low income, being incarcerated or having a close family member die recently,” according to CNBC.

The primary reason for the decline in Obamacare fines last year appears to be that millions of Americans experienced a significant drop in income, which ironically is a direct result of the economic damage inflicted on businesses by the financial strictures of the Obama ‘Affordable’ Care Act (ACA).

CNBC also reported that the new Republican-led Congress last month began taking steps toward repealing key parts of the ACA, which include the funding of premium subsidies and the individual mandate. For the middle class’s economic sake, let’s hope the effort is successful.

The National Taxpayer Advocate has released their 2016 Annual Report to Congress. The report contains data regarding Obamacare premium tax credits (PTC) and individual shared responsibility payment (ISRP) filings – The Obamacare tax penalties for not having health coverage.

The report identifies a number of issues that the IRS has faced or is facing involving the Obamacare ACA and makes a number of recommendations. These include:

- The IRS seems to have largely addressed early problems of Obamacare tax overpayments through outreach conducted to tax practitioners and software providers.

- Reconciliation of PTCs (the Obamacare low-income subsidies) with advance PTCs (APTCs) continues to cause problems, and has risen to the fourth highest category of Taxpayer Advocacy Service cases, accounting for nearly 11,000 cases in 2016. The primary problem seems to be the IRS holding up processing of returns when taxpayers fail to file a form 8962 and reconcile their advance PTC with their PTC.

- Processing of tax filings is delayed when Obamacare APTC recipients incorrectly file form 1040-E, which does not allow for APTC reconciliation.

- The IRS is taking action to address “silent returns,” which do not either check the box indicating full-year coverage, claim an exemption, or paying the ISRP tax penalty. The IRS will send a letter 12C requesting more information in these cases and assess the ISRP if no response is forthcoming.

- The Taxpayer Advocate recommends that the IRS should ease the burden on individuals claiming the religious exemption by allowing individuals exempt from the Social Security and Medicare taxes to simply indicate this on their form 8965 rather than requiring them to apply separately for an Obamacare ISRP religious exemption.

- The Taxpayer Advocate recognizes that taxpayers who receive large Social Security Disability Payments may have to repay Obamacare APTC subsidies they received. There is no apparent administrative fix for this problem.

- The IRS needs to provide specialized training to its newly established Obamacare ACA Business Exam unit, which handles employer ACA returns.

- The IRS may not be adequately prepared to handle Obamacare ACA employer filings. It had expected 77 million 1095-Cs for 2016 and received 104 million or 35% more than expected. Of these Obamacare employer filings, 5.4 percent were then rejected.

The IRS, in a statement regarding taxpayer compliance issues has said: “The IRS will follow its normal compliance approach to filed tax returns. During its normal processes, the IRS routinely follows up on the accuracy and completeness of tax returns and may ask taxpayers to substantiate the information on their tax returns. These inquiries sometime occur before processing refund requests and other times after the processing of refund requests.”

“The vast majority of taxpayers voluntarily comply with their tax responsibilities—our income tax system is built on voluntary compliance,” the IRS said.

* * * * * * * * * * * * * *

At Health Insurance 4 Everyone, we not only want to improve our customer service but also interact with our customers on a social media level that was not available before. Interested in connecting with us? Look us up on….

Twitter: Healthinsurane4

Click-On for LinkedIn: LinkedIn

Like us on facebook: HealthInsurance4Everyone

Follow Mark Shuster, Founder/Owner at Health & Life Solutions, LLC for daily health tips! HealthInsurance4Everyone or Health & Life Solutions, LLC

Mark Shuster FaceBook Link

Follow our word press blog and read about everything from health insurance and reform news to healthy living and current events!

Company Blogs

Find out more about LegalShield, our corporate partner which gives you the power to talk to an attorney about any legal issue, and offering high-quality Identity Theft plans.

Read more