Daily HI4E.org Trivia Contest Winners For The Week Ending: Sunday, December 1st, 2019.

In an effort to broaden the company’s “social interaction” with our clients and FaceBook fans, Daily Trivia Questions are posted on both of our business pages. Here are the weekly standings for this past week, and the winner of the Sunday night Weekly Drawing for an AmEx/VISA gift card!

Congratulations – To this past week’s Trivia Contest Winner!! Our latest contest winner for the weekly FaceBook HealthInsurance4Everyone/Health & Life Solutions, LLC Trivia Contest, drawn randomly by computer late Sunday evening, December 1st, 2019 was:

ANDREA SOMERS

Winner Of A $25.00 AmEX/VISA Gift Card

Each day, fans who have “liked” either of our company FaceBook pages (HealthInsurance4Everyone or Health & Life Solutions LLC) are able to test their skills with our Daily TRIVIA QUESTION. The first 20 winners who post the correct answer to the TRIVIA QUESTION, will then get entered into the weekly drawing held late on Sunday evenings for a $25.00 Am Ex/Visa Gift Card.

Weekly Gift Card winners will be posted in our blog at this site. Remember to become a FaceBook fan and “Like and Follow” either of our company pages to enter and post your answers.

The drawing entries 11/25/19 thru 12/1/19 are:

11/25/19

Andrea Somers

Suzie Mize Lockhart

Amanda Reid

Barbara Austin

Jane Peterson

Brandi K Chaney

Dawn Marie

Lena Perry

Amanda Rosario

Kristina Harris

Kim Avery

Dawn Raasch

Deborah Thomas

Terry Schmitt Sutton

Marilyn Wall

Cathy Ahner

Tracy Heyer

Cheryl Stoker Hall

Steve Ahner

Stephen Earl

11/26/19

Andrea Somers

Joanie Waterman

Lauren Bradley

Melinda Poullion

Dale Fish

Jill Nauyokas

Shannon Schleif

Trish Hysell

Nitasha Shank

Pamela White Brearley

Debbie Bloxom

Tony L Smoaks

April Ashcraft

Karen Brunet Moore

Wendi Black

Rhonda Grisham

Tracy Heyer

Kimberly Taylor Hall

Debbie Garretson

Haley Babineau

Madeline Lonergan

11/27/19

Nicole Blaha

Theresa Signourney

Sheila Carvell

Sherry Lilly

Brittany Doerfler

Patricia Oehlert Vazquez

Melinda Poullion

Andrea Somers

Debbie Garretson

Maria Bouchard

Alicia Dansby

Thomas Ryan Gan

Andrea Ayala

Jenifer Garza

Gina Rock

Danyel Leigh Walentin

Wendi Black

Tina Auth

Amy Flecknoe Moyer

Sarah Bellestri Shih

Alana Dimambro

Karyn Koehler

Dawn Raasch

11/28/19

Wendi Black

Katie Santos

Alyssa DiFazio

Chantal Bell

Kendra Lynne Ramsey

Katrina Jordan-Worford

Jessica Steiner

Jennifer Ramlet

Adaria Johnson

Tiffany Borek

Crystal Young

Becky VanGinkel

Chandra Beckwith

Dave Miller

Melissa Ann Stura-Bassett

Sheila Carvell

Jennifer Vega

Robin Griffitts Pratt

Jean Simmons Homfeld

Lisa Marie Ferraiolo Whitener

Lori Capobianco

11/29/19

Shannon Scott

Jennifer Ramlet

Vickie Gipson

April Ashcraft

Melinda Poullion

Barbara Austin

Dean Bruss

Alana Dimambro

Mandi Smith

Andrea Somers

Brooke Shelby Rae

April Ashcraft

Joann Tompkins-Winborn

Deidra Dees

Misty Shallcross

Mya Murphy

Debbie Gremlin

Kendra Lynne Ramsey

Jennifer Marie

Alyssa DiFazio

Marilyn Wall

Brittany Seiler

Derek Jennings

11/30/19

Martha Prescott

MarTez Rodgers

Karen Bondehagen

Sarah Bellestri Shih

Cathy Ahner

Eleazar Ruiz

Steve Ahner

Christy Hawkes

Barbara Austin

Stephen Earl

Nancy Pfirrman Schools

Rhonda Grisham

Kim Avery

Jay Robert

Bryan Jared

Mike Wallace

Jeannie Prosser

Debbie Bloxom

Cindy Quisenberry

Karen Brunet Moore

Robin Jedele

Jeremy Mclaughlin

12/1/19

Nelle Bailey

Stephanie Beckwith

Tracy Shafer

Janice McKay Donahue

Amanda Rosario

Kassie Lynn DiFazio

Jenai Merri

Kimberly Snyder

Amanda Justice

Tiffany Greene Elliott

Holly Cajigas

Kristina Harris

Sarah Harrison

Donna Blankenship

Anna Nichols

Debbie Gremlin

Melissa White

Jennifer Lang

Marilyn Wall

Debbie Bloxom

Melissa Ann Stura-Bassett

Tammy Lee Stookey

Be sure to watch both of our FaceBook pages for your chance to win and enter again next week, with questions posted daily on HealthInsurance4Everyone or at Health & Life Solutions, LLC!!

Remember that if you try your hand at answering the Trivia Question several days each week, your odds of winning the Sunday weekly drawing are much better.

Also note that a number of the posted answers each day are from contestants who have forgotten to “Like” one of our pages, so their names WILL NOT be entered at the end week drawing for the gift card, giving our fans a better chance!

You may also find that if you “Like” BOTH of the business pages, you will receive faster notifications of the other players as they post their answers to compete with you!

—————————————————————-

At Health Insurance 4 Everyone, we not only want to improve our customer service but also interact with our customers on a social media level that wasn’t available before. Interested in connecting with us? Look us up on….

Twitter: Healthinsurane4 (Follow Us On Twitter To Receive Faster Notifications When Daily Trivia Questions Posted, & To Be Immediately Notified When Weekly AmEX Gift Card Winners Are Announced!!)

Click-On for LinkedIn To Follow Our Posts: LinkedIn

Like us on facebook: HealthInsurance4Everyone or Health & Life Solutions, LLC

Over 54,000 Combined Fans/Followers To Our Social Media Sites, & We’re Growing Daily!

Follow Mark Shuster, Founder/Owner at Health & Life Solutions, LLC for daily health tips!

Mark Shuster FaceBook Link

Follow our word press blog and read about everything from health insurance and reform news to healthy living and current events!

Company Blogs

Find out more about LegalShield, our corporate partner which gives you the power to talk to an attorney about any legal issue, and offering high-quality Identity Theft plans.

LegalShield

Read more

These Five (5) Questions May Hold The Answer….

Going without coverage can be tempting and even seem necessary at times, especially when you are relatively young, relatively healthy and on a relatively tight budget. However, skipping major medical coverage can also be a potentially costly decision. You may wind up owing a tax penalty (yes, even now that the Trump Administration is in office), paying unexpected medical bills out of pocket, or both.

If you are asking yourself if you really need insurance, the answers to these five questions may help you decide.

If you are asking yourself if you really need insurance, the answers to these five questions may help you decide.

1. Are you exempt from the ACA’s individual mandate?

The Obama ‘Affordable’ Care Act’s individual shared responsibility provision (aka, the individual mandate) requires most Americans to have a health plan that qualifies as minimum essential coverage. This may include, but is not limited to, job-based coverage, major medical plans purchased on and away from the state-based and federally facilitated health insurance exchanges, Medicaid and most types of TRICARE (veterans) coverage.

However, exemptions from the mandate are granted to individuals in certain circumstances, including those with coverage gaps of less than three consecutive months, those for whom coverage costs more than a certain percentage of their household income, those with incomes below the filing threshold and others facing general hardship, to name a few.

If you are not exempt and do not obtain coverage as required by the law you could face a penalty known as the shared responsibility payment at tax time.

What could being uninsured could cost you if you’re not exempt?

You may owe a tax penalty known as the individual shared responsibility payment. Those who went without minimum essential coverage in 2016 could face penalties as high as follows: that penalty could be as high as :

- 2.5% of their annual household income above the tax filing threshold to a cap of the national bronze plan s premium, or

- $695 per adult and $347.50 per child under 18 to a maximum penalty of $2,085 per family.

For every month that you are uninsured and not exempt, you owe 1/12 of the annual shared responsibility payment.

In 2017 and beyond, the penalties remain the same, but will be adjusted for inflation.

2. How will you pay for healthcare if you need it?

While we know it can happen, we never really plan on becoming ill or getting injured, especially when our medical histories are relatively spotless. If you have no benefits to help with covered expenses when you do get sick or hurt and need medical care, you will have to pay 100% of the bills out of pocket. Whether your healthcare expenses are expected or not, do you have access to savings, credit or other funds to help pay for healthcare?

What could being uninsured cost you if you need healthcare?

Insurance status has a strong association with medical bill difficulties—more than half of uninsured individuals report problems paying household medical bills. On average, a trip to urgent care will cost $150 and a trip to the emergency room will cost over $1,000. Fixing a broken leg can cost up to $7,500 and the bill for a three-day hospital stay hovers around $30,000.

3. Do you plan on being uninsured for short time?

Accidents and illnesses can happen any time, not just when it is convenient. Even if you are about to start a new job with benefits that kick in a month or two down the road, it is wise to have a plan for how you will pay for healthcare in the meantime.

Short term health insurance plans provide temporary coverage for as few as 30 days. They offer a range of benefits to help with covered expenses, including office visits and emergency care, and they can be quickly obtained. Application and enrollment take only a few minutes, and coverage begins as early as the day after you enroll. You can buy short term coverage year-round.

What could a short term health plan cost you?

Typically, short term plan premiums are a fraction of major medical premiums. Keep in mind that short term plans are not the same as Obamacare plans (i.e., major medical insurance). They are not subject to the ‘Affordable’ Care Act, which means you may be denied coverage based on your health history and, if you are not exempt from the shared responsibility provision, having short term coverage will not prevent you from owing a tax penalty.

If you plan to be uninsured longer than three months and do not qualify for a special enrollment period, you may consider a hospital indemnity plan.

Learn about HIP (Hospital Indemnity Plans)

4. Will you qualify for an Obamacare subsidy?

If you buy a major medical plan from a state-based or federally facilitated health insurance exchange (the Obamacare plans) and meet certain income qualifications, you may be eligible for a subsidy. Obamacare subsidies include advanced premium tax credits that help lower your monthly premium payment.

Remember: You can only buy major medical plans during the annual open enrollment period or during a special enrollment period if you have a qualifying life event.

What could health insurance cost you with an Obamacare subsidy?

Major medical health insurance premiums vary depending on a number of factors, including where you live, what type of plan you choose (i.e., bronze, silver, gold, platinum), and your age. In 2016, the average premium for health insurance plans purchased through the federal Obamacare HealthCare. gov exchange was $408 per month.

However, 83% of people who purchased healthinsurance through HealthCare. gov received subsidies that helped lower their monthly premiums. The average advanced premium tax credit amount was $294 per month, which lowered the average monthly cost to $113 per month.

Consider “Gap” Insurance To Cover The Higher Obamacare Plan Deductibles & Out-Of-Pocket Limits

5. Are you eligible for Medicaid?

In 2014, Medicaid eligibility was expanded to include single adults earning up to 133 percent of the federal poverty level. Not all states decided to participate in this optional expansion. You can enroll in Medicaid year-round. To view your state’s eligibility criteria, click here to visit Medicaid.gov’s State Medicaid & CHIP Profiles page.

What could Medicaid coverage cost you?

If you qualify for Medicaid, you may be able to get low-cost or no-cost coverage.

The Obama ‘Affordable’ Care Act may require you to buy health insurance, and there may be financial risks in going without it. Ultimately, you must decide if you need health insurance. It is important to understand all of the benefits and risks associated with your decision. Work with a health insurance producer to determine the right coverage  options for your health and financial situation.

options for your health and financial situation.

You can call the number at the top of your screen to speak with a certified advisor (i.e., health insurance producer) who can assist you. You can also obtain quotes for supplemental products, short term coverage and off-exchange Obamacare plans at :

HealthInsurance4Everyone – www.hi4e.org

Read more

In a press conference earlier in January, to announce the start of the 2017 tax filing season, which began on Jan. 23rd, the IRS said it expects more than 153 million tax returns this year.

More than 70% of taxpayers will receive a refund in 2017, with 90% or more of refunds issued in fewer than 21 days after returns are submitted, the IRS estimated. In 2016, 111 million individual tax refunds were issued.

Most filers who received government subsidies to buy Obamacare state exchange plans had to pay money back to the IRS last year, according to an H&R Block analysis released in 2016 that looks at the health law’s two full tax seasons. If a taxpayer projected a higher annual household income than they actually claimed in their filing, they may owe tax credits back that they received by purchasing an Obamacare policy or their state’s exchange plan. One other cause for having to repay tax credits is due to claiming eligibility, but not being eligible due to having access to affordable employer coverage.

The tax-prep giant studied its own massive customer base and concluded that two-thirds of its filers who got subsidies from Obamacare were overpaid during the course of the year, and owed money back to the IRS on the April 15th deadline.

The ‘Affordable’ Care Act, better known as Obamacare, mandates Americans — unless they’re qualified for an exemption — to carry health insurance coverage or pay a penalty when filing their tax returns. The IRS says most taxpayers simply need to check a box to verify that they have insurance. For others with more complex answers, the agency offers tips on IRS.gov/aca.

IRS Commissioner John Koskinen said the number of people receiving Obamacare subsidies during the last tax season (2015 tax filing), was up from 3 million in 2014. For that year, customers got more than $10 billion in tax credits, with an average subsidy of $3,430 annually, according to the IRS. Obamacare subsidies are available to wage earners with low and moderate incomes. People who earn less money get more in assistance than higher earners.

Koskinen wrote that about 6.5 million taxpayers last tax season reported owing a total of $3 billion in such tax penalties for failing to have coverage in 2015. In contrast, about 8 million people owed an Obamacare fine for lack of coverage in 2014. Fines related to lack of coverage in 2014 totaled $1.6 billion.

CNBC reported that some 12.7 million people claimed one or more exemptions from the ACA-coverage mandate when they filed their taxes last year. “The exemptions are wide ranging and can include having very low income, being incarcerated or having a close family member die recently,” according to CNBC.

The primary reason for the decline in Obamacare fines last year appears to be that millions of Americans experienced a significant drop in income, which ironically is a direct result of the economic damage inflicted on businesses by the financial strictures of the Obama ‘Affordable’ Care Act (ACA).

CNBC also reported that the new Republican-led Congress last month began taking steps toward repealing key parts of the ACA, which include the funding of premium subsidies and the individual mandate. For the middle class’s economic sake, let’s hope the effort is successful.

The National Taxpayer Advocate has released their 2016 Annual Report to Congress. The report contains data regarding Obamacare premium tax credits (PTC) and individual shared responsibility payment (ISRP) filings – The Obamacare tax penalties for not having health coverage.

The report identifies a number of issues that the IRS has faced or is facing involving the Obamacare ACA and makes a number of recommendations. These include:

- The IRS seems to have largely addressed early problems of Obamacare tax overpayments through outreach conducted to tax practitioners and software providers.

- Reconciliation of PTCs (the Obamacare low-income subsidies) with advance PTCs (APTCs) continues to cause problems, and has risen to the fourth highest category of Taxpayer Advocacy Service cases, accounting for nearly 11,000 cases in 2016. The primary problem seems to be the IRS holding up processing of returns when taxpayers fail to file a form 8962 and reconcile their advance PTC with their PTC.

- Processing of tax filings is delayed when Obamacare APTC recipients incorrectly file form 1040-E, which does not allow for APTC reconciliation.

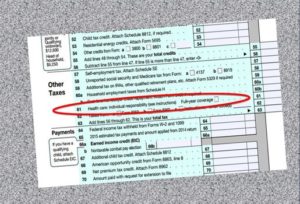

- The IRS is taking action to address “silent returns,” which do not either check the box indicating full-year coverage, claim an exemption, or paying the ISRP tax penalty. The IRS will send a letter 12C requesting more information in these cases and assess the ISRP if no response is forthcoming.

- The Taxpayer Advocate recommends that the IRS should ease the burden on individuals claiming the religious exemption by allowing individuals exempt from the Social Security and Medicare taxes to simply indicate this on their form 8965 rather than requiring them to apply separately for an Obamacare ISRP religious exemption.

- The Taxpayer Advocate recognizes that taxpayers who receive large Social Security Disability Payments may have to repay Obamacare APTC subsidies they received. There is no apparent administrative fix for this problem.

- The IRS needs to provide specialized training to its newly established Obamacare ACA Business Exam unit, which handles employer ACA returns.

- The IRS may not be adequately prepared to handle Obamacare ACA employer filings. It had expected 77 million 1095-Cs for 2016 and received 104 million or 35% more than expected. Of these Obamacare employer filings, 5.4 percent were then rejected.

The IRS, in a statement regarding taxpayer compliance issues has said: “The IRS will follow its normal compliance approach to filed tax returns. During its normal processes, the IRS routinely follows up on the accuracy and completeness of tax returns and may ask taxpayers to substantiate the information on their tax returns. These inquiries sometime occur before processing refund requests and other times after the processing of refund requests.”

“The vast majority of taxpayers voluntarily comply with their tax responsibilities—our income tax system is built on voluntary compliance,” the IRS said.

* * * * * * * * * * * * * *

At Health Insurance 4 Everyone, we not only want to improve our customer service but also interact with our customers on a social media level that was not available before. Interested in connecting with us? Look us up on….

Twitter: Healthinsurane4

Click-On for LinkedIn: LinkedIn

Like us on facebook: HealthInsurance4Everyone

Follow Mark Shuster, Founder/Owner at Health & Life Solutions, LLC for daily health tips! HealthInsurance4Everyone or Health & Life Solutions, LLC

Mark Shuster FaceBook Link

Follow our word press blog and read about everything from health insurance and reform news to healthy living and current events!

Company Blogs

Find out more about LegalShield, our corporate partner which gives you the power to talk to an attorney about any legal issue, and offering high-quality Identity Theft plans.

Read more